Sharper Risk Insights for Underwriting

Protect your book with more visibility and insight into risks with safety management software

Mitigate loss and reduce claims

Reduce TCOR by addressing leading indicators of risk.

Solidify your leadership position

Attract and retain clients by offering the latest in AI safety.

Visibility

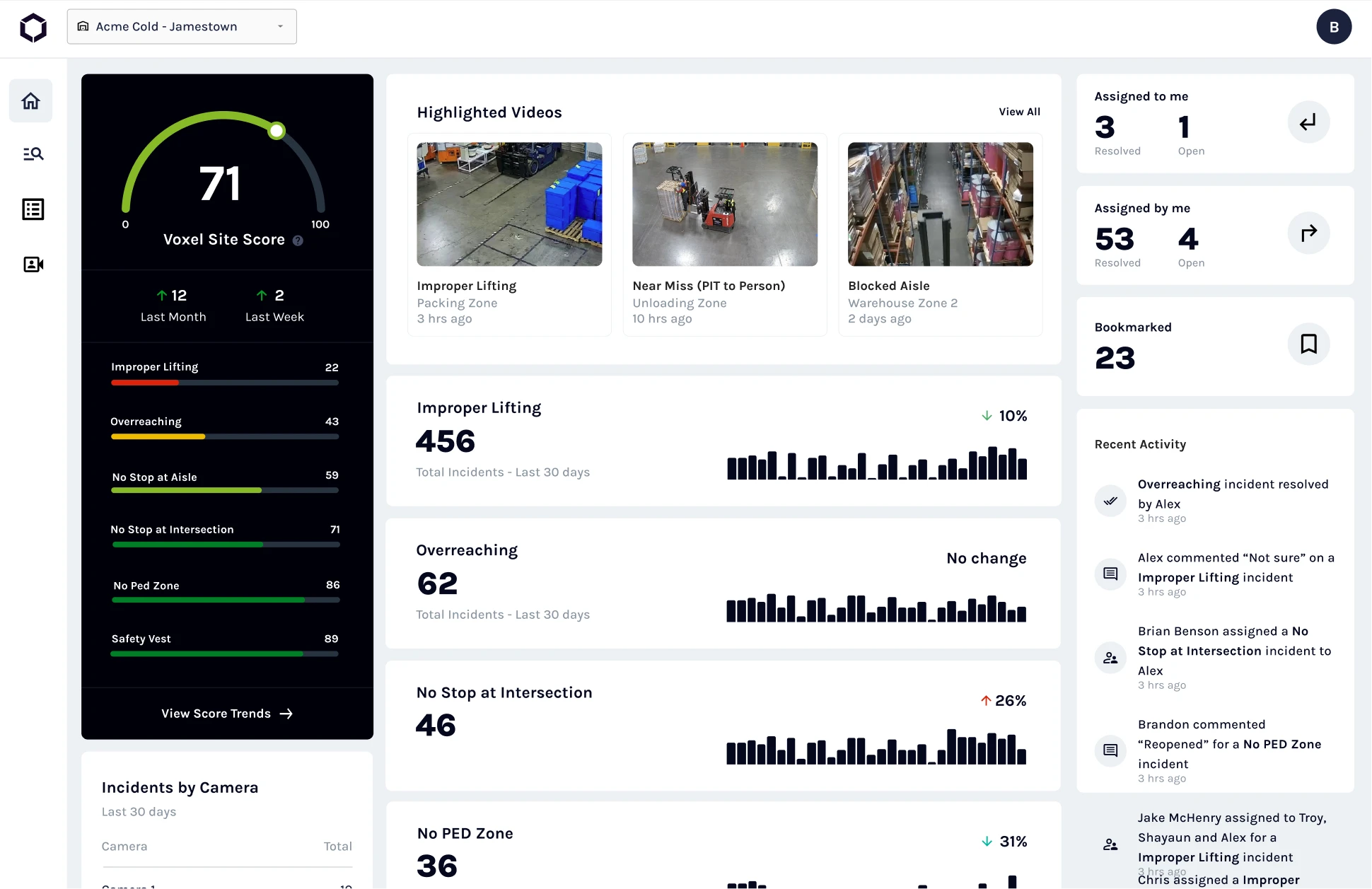

Risk understanding, revolutionized

Voxel gives a comprehensive view into where, when, and how often risks occur, empowering your underwriting decisions.

Insights

Confidently develop and deploy risk control plans

Use leading indicator data to measure and manage effective mitigation strategies.

Growth

Attract and retain business

Introducing transformative safety innovations like Voxel to your clients reduces risk and elevates your competitive edge.

Partnering with Voxel, Safety National innovatively addressed risk for a national retail client. Our client saw significant improvements in safety behaviors, enhanced operational efficiency, and they reduced recordable injuries. Voxel played a key role in delivering remarkable success for all stakeholders involved."